The expectations and future of LP investing is changing.

Note from Ryan Hoover: Today, we’re publishing a guest post from Pavel Prata from Murph Capital.

Depending on where one draws the starting line, the venture capital industry has existed for more than 60 years. But for most of that time, its underlying model was surprisingly simple. Venture funds existed to underwrite risk – accepting uncertainty in exchange for power-law outcomes, where a single company could return an entire fund.

The mechanics were clear. VCs raised capital from LPs, sourced companies, selected founders, and competed for access. We can debate endlessly how much skill versus luck this required, but one thing is indisputable: none of it was possible without capital itself.

Until the early 2000s, venture capital functioned less like a partnership and more like a transaction. VCs behaved closer to risk-tolerant bankers – underwriting unproven business models and unconventional founders, largely thanks to information asymmetry. The relationship was straightforward: here is the capital – call us again at the liquidity event.

At that time, the idea of “value-add” barely existed – at least not in the modern sense. The most meaningful help a VC could offer was largely transactional: introductions to local law firms, accountants, or, at later stages, investment banks preparing an IPO. Operational involvement was minimal. The assumption was that capital itself was the scarce resource – and therefore the differentiator.

Looking back, it’s clear that this assumption began to erode earlier than most people realized. Not because venture firms consciously changed their philosophy, but because the underlying market conditions no longer supported it.

At Murph Capital, we've been thinking about this shift from the LP side – specifically, what it means for how allocators should operate today. We believe the value-add model that transformed venture capital is now playing out one layer up, and that most of the industry hasn't caught up yet. This essay is our attempt to dig into why.

The Dot-Com Crash

The first crack appeared with the dot-com bubble:

- In the late 1990s, U.S. VC funding peaked at $105 billion – the highest ever. By 2002, it had cratered 96% to $4.2 billion.

- Venture IPOs froze (from 159 in 1999 to 7 in 2002), starving exits and torching LP trust.

- Many pre-bubble funds wrote off 80–90% of their portfolios. Fly-by-night GPs fled the scene.

But the more durable consequence wasn’t financial. It was reputational.

A meaningful number of funds (raised on a “everyone else is doing it” mentality) reacted poorly under stress. Some abandoned portfolio companies. Others restructured aggressively in ways that prioritized fund survival over founder outcomes. Founders started to distinguish between firms not just based on returns, but based on behavior under pressure. Those impressions carried forward from one generation of founders to the next.

This still wasn’t “value-add” in the modern sense. What changed was perception and memory, not yet infrastructure or support. But it planted the seed.

Startup Costs Collapse

Around the same time, a slower shift was unfolding – one with longer-term consequences for the entire industry.

Between 2003 and 2013, the cost of building a technology company collapsed:

- AWS launched in 2006

- GitHub arrived in 2008

- Stripe, Auth0, and a wave of SaaS abstractions replaced expensive on-premise infrastructure with pay-as-you-go building blocks

- A product that cost $3–5 million to build in 2000 could be built for $100–500K a decade later

- Startup formations exploded: U.S. new firms rose rapidly, while VC AUM rebounded to $74.1 billion by 2014

The result was an inversion that had never existed before. More capital was flowing into venture at the same time that founders needed dramatically less of it. Under these conditions, it became increasingly difficult for venture firms to differentiate themselves purely through access to capital.

For the first time at scale, strong founders began selecting their investors – not just the other way around.

The Rise of the Value-Add Model

Faced with capital commoditization, venture firms were forced to adapt. The goal shifted from simply deploying capital to consistently winning the first pick of each generation of startups. Brand became a strategic weapon. And the most reliable way to build a brand was to give founders something they actually needed.

Paul Graham articulated the insight simply when YC launched in 2005: the bottleneck isn’t capital. It’s knowledge, confidence, and network.

YC’s initial model looked almost trivial on the surface – small checks (initially around $20,000), batch structure, weekly office hours, Demo Day. But over time, the alumni network compounded. Early portfolio success reinforced brand. Brand improved sourcing. Better sourcing improved outcomes. The flywheel was self-reinforcing, and capital was explicitly secondary to it.

But there are some other great examples which I also mentioned in my essay about new VC/LP media:

- First Round Capital (2004): First institutional seed player. Ex-founder partners focused on the “first 18 months” – hands-on product, GTM, fundraising. Built founder communities, content (e.g., the 10-Year Review), and specialists in sales, recruiting, and ops. Thesis: win early by being indispensable.

- Andreessen Horowitz (2009): Launched with a lot of skepticism from fellow VCs, but built from day one on the belief that capital was commoditized and platform was the product. Reinvested 20–30% of management fees into operators across recruiting, PR, BD, and policy. By 2026, expanded into a16z Build, new media, originals, and community — a full ecosystem lock-in strategy that turned the firm into the biggest brand in venture.

The rest of tier one:

- Bessemer built an entire public benchmark around its franchise – the BVP Cloud Index, launched in 2013 which over a decade became the de‑facto market barometer for public cloud companies and a powerful top‑of‑funnel magnet for SaaS founders.

- Union Square Ventures leaned into its network thesis, cultivating internal communities across portfolio companies and turning the portfolio into a learning network.

- SignalFire invested heavily in data infrastructure: by the mid‑2020s its internal talent and market data platform tracked hundreds of millions of professionals and tens of millions of organizations, turning sourcing and talent support into a product‑like advantage.

- NFX built a media and frameworks engine around network effects, publishing playbooks and tools that made the firm synonymous with a particular way of building software businesses.

Capital had become the price of admission. Value-add was the actual product.

GPs Are Also Founders

But why am I writing all of that?

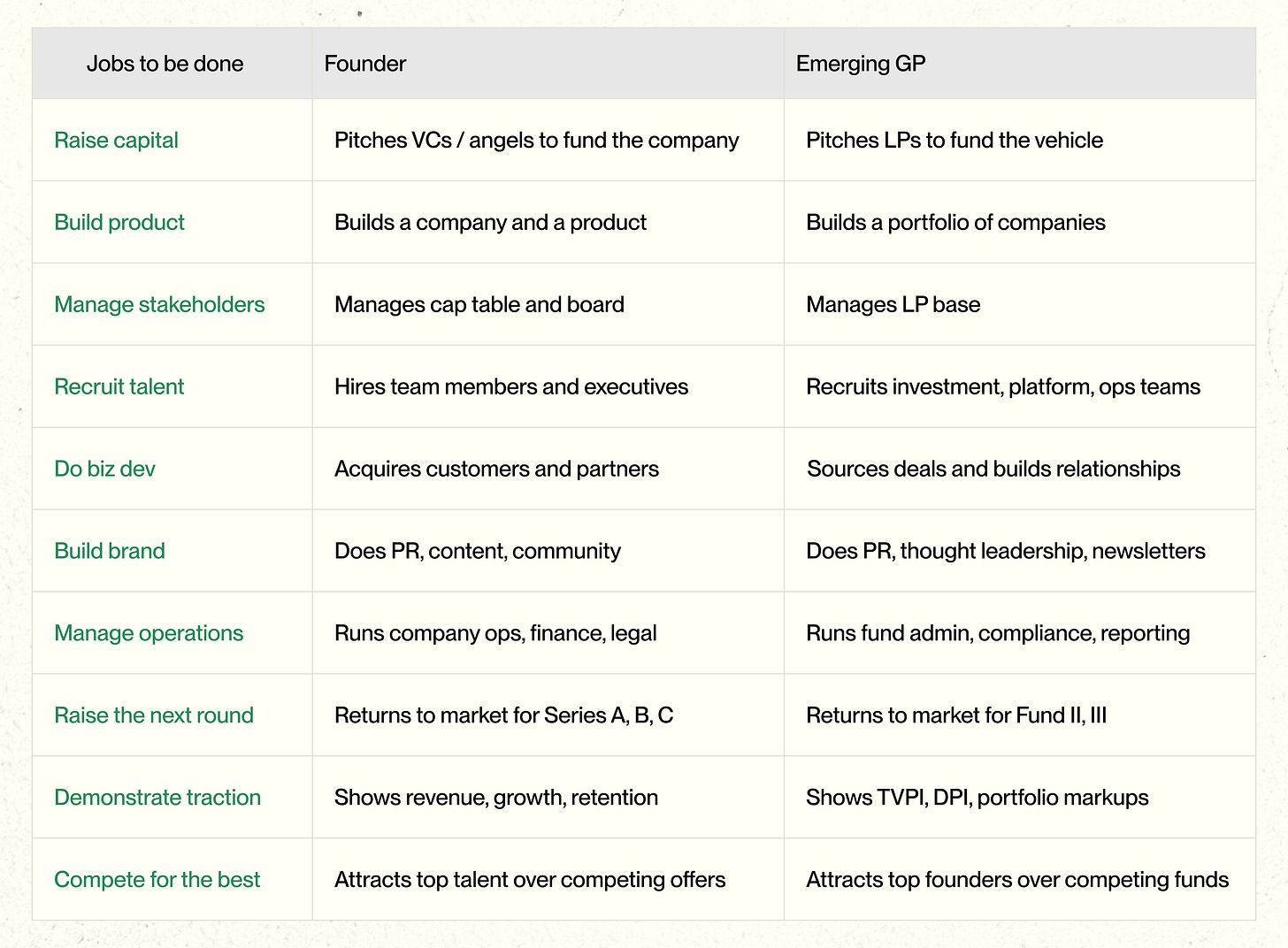

Because today’s emerging managers increasingly resemble founders – they simply operate a different kind of company. Instead of building a product and acquiring customers, they build a fund and attract capital. The underlying mechanics are surprisingly similar.

And just as the startup ecosystem changed dramatically over the past two decades, the ecosystem of venture managers has changed with it. Several structural shifts have quietly altered both who becomes a GP and what the job actually requires.

- Access to venture investing is democratizing. Launching an investment vehicle has become significantly easier. Infrastructure platforms, scout programs, rolling funds, SPVs, and fund-administration services have reduced the operational friction of starting to invest.

- Regulatory changes. the JOBS Act, Rule 506(c) – loosened the historically closed nature of private fundraising networks. What previously required years inside an established venture firm can now begin with smaller vehicles and incremental experimentation.

- Companies stay private longer while private-market capital expands. Over the past decade, venture-backed companies have increasingly delayed IPOs. Global private market AUM crossed $13 trillion by 2023. Much of the value creation that previously occurred in public markets now happens while companies are still privately held. More startups are being built, more capital is chasing them, and more investors believe they have a chance to participate in power-law dynamics. Naturally, this attracts a growing number of new venture managers.

- The archetype of the venture capitalist has changed. Today’s emerging managers increasingly originate from the same environments as the founders they back. Engineers, operators, researchers, product leaders, media personalities, and community builders are launching funds built around the networks and domains where they already have credibility. A former Palantir engineer launching a defense-tech fund may have far stronger credibility with early founders in that domain than a traditional generalist partnership. An operator from Stripe often raises within communities where they already possess trust and informational access that no established firm can replicate.

But this shift introduces a structural tension. The skills required to generate leverage for founders (domain knowledge, network access, distribution, credibility) are not the same skills required to build and operate a venture firm.

Fund construction, LP relations, compliance, reporting infrastructure, and long fundraising cycles demand a completely different operating discipline. Being a great domain expert doesn’t make you a great fund builder.

This creates a noticeable asymmetry inside the ecosystem.

Over the past 15 years, the venture industry has normalized the expectation that GPs should provide meaningful value to founders beyond capital. Founders actively select investors based on the leverage they can provide.

Yet on the LP side, the relationship has changed much less. In many cases, the model still resembles the older version of venture capital itself: capital is committed, performance is expected, and the relationship remains relatively passive.

The Counterargument Everyone Raises

When I share this thesis – that LPs should be more actively supportive of their GP portfolios, the way GPs became more actively supportive of their founder portfolios – the pushback is predictable.

Venture is a fiduciary business, the argument goes. Capital gets deployed regardless. GPs take checks from whoever shows up with the right terms. The relationship between an LP and a GP isn’t a coaching relationship – it’s an investment relationship, governed by fund documents and fiduciary duty.

It’s a fair objection. And it’s the same objection that a certain kind of VC was making in 2005, right before First Round / YC made it irrelevant.

So why LPs should support GPs beyond capital?

Reason #1: Unfair Leverage

The “money is money” argument sounds compelling until you look at how the best founders actually behave when they have options.

A founder raising a round doesn’t need every investor – they need a fixed amount of capital. And when a round is oversubscribed, the founder isn’t asking who will write the check. They’re asking who will make the check worth more than its face value.

Because in venture, time is IRR. Every month it takes to close an enterprise deal, hire a key executive, or raise the next round is a month of compounding that doesn’t happen. The right investor doesn’t just fund the journey – they compress it.

When a credible brand like a16z leads a round, something interesting happens: the founder’s inbox fills instantly with inbound interest from other investors. The round moves faster. The founder returns focus to building rather than fundraising. That’s not capital doing the work. That’s leverage.

If everything works as intended, the sequence looks like this:

- A startup is a business whose objective is to increase enterprise value

- The investor provides leverage – customers, talent, distribution, capital access

- That leverage accelerates growth and improves fundamentals

- Stronger fundamentals increase valuation

- A higher valuation ultimately benefits both founders and investors at exit

Investor support is not about rescuing a weak founder. It’s about accelerating a strong one.

Now look at where a GP’s time actually goes: based on my conversations with emerging managers, in today’s market sub-$100M funds spend roughly 40% of their time on fundraising and investor relations alone (where the average fund takes 17.8 months to close). The rest gets split between LP reporting, fund administration, legal and compliance, portfolio monitoring and of course – finding and backing founders.

So the logic is identical one layer up (founders → VCs → LPs). When time is IRR, anything that compresses the timeline compounds.

If an LP accelerates some of these functions (introductions to other LPs, back-office setup, narrative and positioning, distribution support) the GP gains something extremely valuable: time. Time that can be reallocated to working with founders and identifying the right companies. If that leverage works properly, the sequence looks like this:

- The fund closes faster, and closer to its intended target size – allowing the manager to construct the portfolio it was designed to be, rather than adjusting strategy to fit whatever capital came together.

- Clear positioning and storytelling increase the manager’s visibility, making it easier to attract strong founders and communicate the fund’s edge.

- Operational infrastructure reduces the time the GP spends running the firm itself.

- The GP sees more deals, from a broader surface area, and can select companies with stronger GP–founder fit.

- More time with founders allows the GP to do the part of the job that actually compounds: helping portfolio companies grow.

- And finally this compounds the way it describes above.

So we have the same case: a hands-on LP isn’t fixing weak managers. They’re accelerating the strongest ones.

Reason #2: AI And The Information Asymmetry Collapse

Sourcing

Another force is reinforcing this dynamic: the rapid rise of AI and the gradual collapse of information asymmetry.

Late last year I came across an essay by Ryan Hoover titled “All That Matters Is Winning.” One of the central ideas: in a world of increasingly powerful tools, “everyone will see every deal,” and machines will often process and evaluate opportunities faster than humans. The implications extend directly to the LP ecosystem.

At the startup level, founders now operate in a world of extreme visibility. Companies launch on Product Hunt, build audiences on X, publish progress publicly, and leave digital traces across dozens of platforms. Tools like Harmonic, Pitchbook, Landscape, and Tracxn attempt to structure this chaos into searchable datasets.

Yet most of these tools become effective only after a company begins generating signals – users, revenue, hiring, or funding rounds. At the earliest stage, when a company is still little more than an idea and a small group of people, the signal is almost invisible. That early darkness is precisely where early-stage funds and angels operate.

The fund side looks meaningfully different – and for a structural reason.

- There’s no vibecoding in fund management. You can’t build in stealth. The moment you raise outside capital, you become visible.

- Startups operate in a regulatory vacuum. Funds don’t. Managing outside capital means filing Form D with the SEC after a first close – a public, timestamped record of the fund’s existence, target size, and early fundraising activity.

In practice, many allocators already scrape these filings and combine them with other public signals to track the emerging manager landscape. The fund ecosystem is, in many ways, far more observable than the earliest stages of the startup ecosystem itself.

Diligence

The diligence process is also being restructured. Evaluating emerging managers tends to follow a consistent pattern: a data room containing track record information, fund strategy, portfolio construction model, founder references, and a broader qualitative assessment.

Traditionally, allocators did all of this themselves – manually working through data rooms, building track record models, running references, synthesizing everything into an investment memo. It required time, skill, and expensive proprietary benchmarking data.

Today, allocators operate more like conductors. The machine does the heavy lifting:

- Faster – ingesting data rooms, decks, meeting notes, web presence, social profiles, SEC filings, and reference signals in a fraction of the time a human analyst would need

- Cheaper – Claude Max costs $100/month while a junior analyst costs $150,000/year

- Better – maintaining context across dozens of manager evaluations simultaneously, applying consistent frameworks, and incorporating proprietary datasets that would be impossible to hold in a human’s head

The result is a significant expansion of capacity. An allocator running AI-augmented workflows can evaluate meaningfully more managers per quarter than before.

Winning

But here’s the consequence most people aren’t drawing: when everyone uses the same data to evaluate the same managers, and AI augments everyone’s diligence in roughly the same ways, the informational edge that used to differentiate the best allocators largely disappears.

What doesn’t disappear is access.

Not access in the sense of simply being allowed to invest (although oversubscribed emerging managers increasingly are selective about their LP base).

Access in the sense of seeing the best managers first, before they’re in market, before they’re competitive. Being the LP that a GP calls when they’re first thinking about their next fund – not when they’re already in the middle of their roadshow. Having managers come to you inbound rather than spending cycles on outbound sourcing.

That kind of access isn’t built through better data or faster diligence. It’s built through reputation. Through genuine relationships. Through being the LP that GPs talk about when other GPs ask who’s actually helpful.

Which brings the argument back to the same place venture arrived 20 years ago: in a market where the informational playing field is leveling, the durable edge is the one that compounds through relationships, brand, and demonstrated value.

Do LPs Actually Help GPs?

So what’s actually happening in the market today?

Before looking at this, it’s worth noting that value-add isn’t a requirement for every LP type. VCs are essentially professional company pickers – outsourced selection engines compensated through carry. Their edge comes from full focus on finding startups, and to maximize that edge they need to pick from the widest possible funnel with the strongest possible conviction. Which, as I described above, requires creating value beyond capital.

For LPs, the professional pickers are Fund of Funds. In my view, this is the LP type with both the strongest incentive and the most structural ability to deliver value-add – to maximize inbound from the best managers, and to see them first.

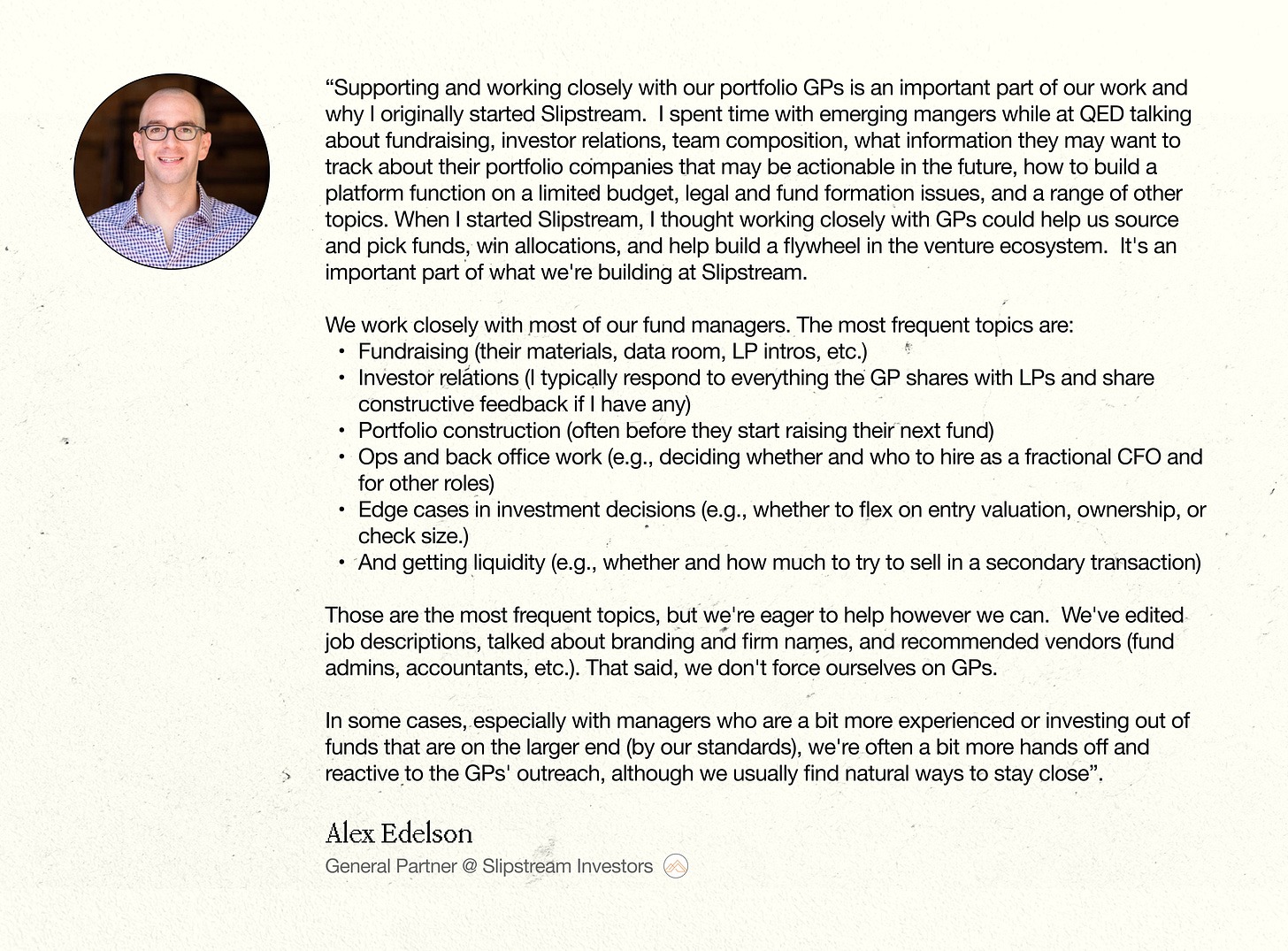

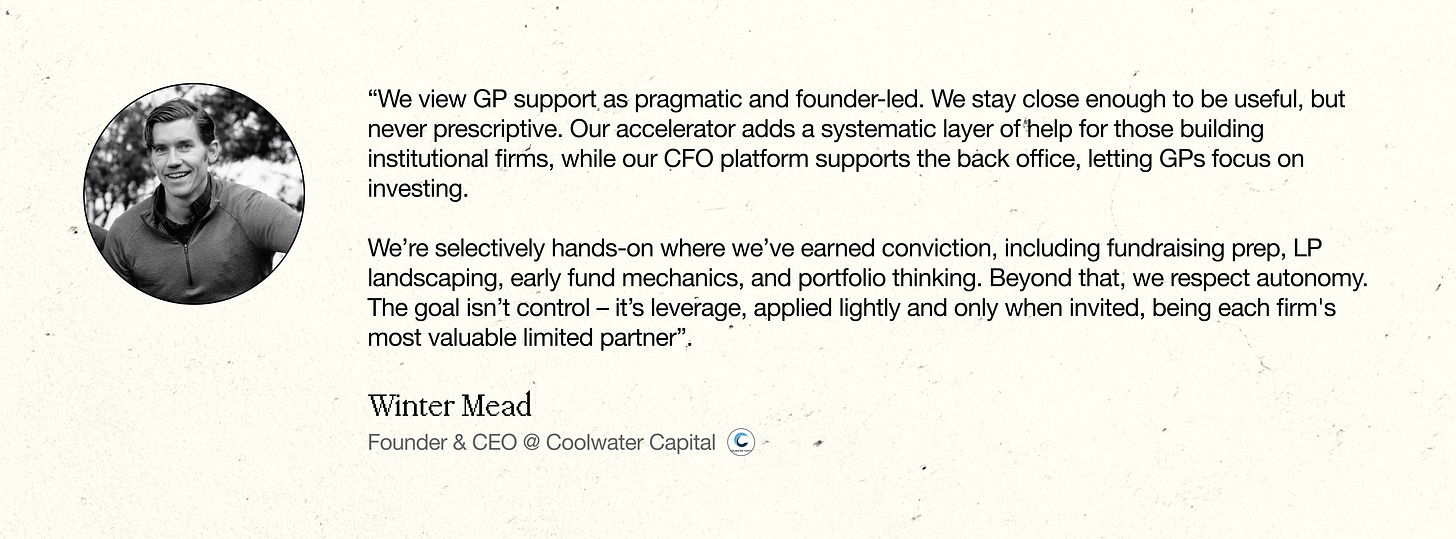

While writing this essay, I reached out to several VC-focused fund of funds to ask what they actually do for their portfolio GPs:

Albert Azout from Level VC

Alex Edelson from Slipstream

Winter Mead from Coolwater Capital

John Felix from Pattern Ventures

Lisa Cawley from Screendoor

Almost every fund of funds that responded to my question supports their GPs in some way. A few of them built their entire model around this idea from day one – Slipstream, Pattern, Screendoor each described GP support not as a nice-to-have but as a core part of why they exist.

The mechanics split into two categories.

- The first is table stakes – things most active FoFs already do to some degree: fundraising support, LP introductions, back office guidance, portfolio construction feedback. Useful, but increasingly replicable.

- The second is proprietary – things that are harder to copy because they’re built on specific infrastructure or relationships. Level VC, for example, processes terabytes of private market data daily and can offer GPs research and data capabilities that most emerging managers couldn’t build themselves.

Looking forward, I think we’ll start to see more FoFs develop value-add that’s genuinely hard to replicate – built around their specific edge rather than a generic support menu, like a16z-style marketing support or distribution-own PR.

The FoFs that build something in this second category — something that’s genuinely theirs — will be the ones that emerging managers talk about. And in this business, being talked about is how you get seen first.

Do All LPs Need to Help?

I think value-add is a logical step, but the honest answer is that it's not structurally available to most LP types. The incentive exists across the board, but the ability to act on it doesn't. Different allocators face different constraints, and most of those constraints are real rather than philosophical.

- Scale. Many LPs don’t have the scale to justify building GP support infrastructure. Even for a FoF with an additional 1% management fee, it’s hard to build a real platform. Supporting managers requires time, people, and organizational focus that may simply not pencil out at smaller AUM.

- Portfolio diversification. For many LPs, VC is just one strategy alongside PE, real estate, and hedge funds. Value-add only makes sense if you’re concentrated enough to benefit from it. If a passive VC check underperforms, real estate picks up the slack.

- Fund size dynamics. Large institutional checks go into large established platforms. Large platforms don’t need value-add from LPs – they’re building their own brand that pulls LPs inbound. Pitching “value-add” to a $30B Anthropic Series G round makes about as much sense.

- Organizational structure. Endowments, pensions, and sovereign wealth funds are built around governance and risk management, not operational engagement. Investment teams have narrow mandates. Fiduciary obligations constrain involvement. Even if individuals inside those organizations wanted to provide deeper support, the institutional framework usually won’t allow it.

Why This Might Change

For a long time, the standard argument from allocators was straightforward: they already add value by providing professional diversification management one layer up – and that’s enough to justify the additional fee layer. Building anything beyond that didn’t make economic sense on a 1% management fee, and frankly, nobody was demanding it.

The market also didn’t force the issue. The number of emerging managers stayed manageable, the number of FoFs stayed manageable, and without a clear leader in either camp, there was no competitive pressure to do more.

That’s changing:

- AI changes the unit economics. AI dramatically expands what a small team can do. Even allocators operating on thin management fee structures an additional 1% on top of the GP’s 2% can now build platform capabilities that previously required the headcount budgets of large endowments. The constraint wasn’t ambition. It was math. AI is changing the math.

- The number of emerging funds will keep growing. More managers entering the market means more competition for alpha among allocators trying to build portfolios that justify an emerging manager strategy over a plain vanilla VC allocation.

- Competition among LPs for the best managers is intensifying. Oversubscribed funds can afford to be selective about their LP base – and increasingly are. In that environment, capital alone may no longer guarantee access. The LP who can provide introductions, credibility, or operational support becomes a more attractive partner than one who can only wire a check.

- More FoFs will connect the dots. The framework a16z built 15 years ago at the GP level is replicable one layer up. The FoFs that figure this out first will build the kind of brand that pulls the best emerging managers inbound – and lets them pick first.

The Proof Will Be in the Numbers

All of this is still largely theoretical. Whether platform allocators become the norm or remain a niche experiment depends almost entirely on what the early movers can demonstrate.

The venture industry didn’t adopt the value-add model because it sounded good in a blog post. It adopted it because YC produced the biggest inbound pipeline in the history of venture, and a16z produced returns – and the data made the argument for them. The same dynamic will play out one layer up.

If the first FoFs that invest seriously in GP support can show that it moves the needle on either of the two things that actually matter in this business – performance and fundraising – the model will spread. If they can’t, it will remain a talking point at LP conferences.

The two core questions are straightforward:

- Does hands-on LP support improve fund returns?

- And does it improve the FoF’s own ability to raise capital?

But how would you even measure this?

The attribution problem is real. If a FoF helps a GP close their fund 6 months faster and that GP goes on to back a breakout company, how much of that outcome belongs to the LP support versus the GP’s judgment versus the market? You can’t run a controlled experiment on vintage years.

Here are some metrics I believe worth to track:

- Fundraising velocity. Do GPs in a platform FoF’s portfolio close faster than comparable managers? Average time-to-close is already benchmarked across the industry.

- Fund size vs. target. Do supported GPs hit their target fund size more consistently? A manager who raises $40M against a $35M target is in a fundamentally different position than one who raises $22M against the same target.

- Inbound vs. outbound deal flow for GPs. Are portfolio GPs seeing more founder inbound over time? Stronger brand and better storytelling should show up in how founders find and approach the fund.

- LP base quality at subsequent funds. Do GPs backed by platform FoFs attract better institutional LPs in Fund II and Fund III?

- FoF’s own inbound. Are the best emerging managers coming to the FoF first, or is it finding out about funds after they’re already oversubscribed? The ratio of inbound to outbound manager sourcing is a reasonable proxy for brand compounding.

- TVPI and DPI vs. peers. Ultimately, the performance has to show up in the numbers. A FoF can track its own returns against Cambridge Associates benchmarks and ask whether vintages with more active GP support outperform those without.

None of these metrics are clean. All of them are worth tracking. The FoFs that start building this data now – even informally, even imperfectly – will be the ones with the strongest argument when the model is inevitably questioned.

Conclusion

- The large venture firms already ran this playbook. And the results are visible. a16z, First Round, YC – each built a center of gravity around their portfolio that compounded into brand, access, and ultimately performance. They didn’t just pick winners. They created conditions that made winning more likely. The firms that did this earliest now sit at the top of every founder’s shortlist by default.

- The emerging manager category is still relatively young. The idea that a dedicated, institutionalized fund of funds focused on emerging managers could itself become a brand (a platform, a center of gravity) hasn’t really been tested yet. Partly because the category only reached critical mass recently, as access democratized and the first generation of emerging managers built track records that became benchmarks. Founders Fund, Thrive Capital – these names are now shorthand for something. The funds that backed them early aren’t.

- The core argument of this essay is simple. Helping portfolio GPs is not about doing their work for them or rescuing the ones who are struggling. It’s about accelerating the best ones – and using that as an unfair advantage to build trust, reputation, and brand over time. That brand, once built, does something specific: it increases the volume of inbound from strong managers, and it ensures you see them first. In an era where sourcing and diligence are increasingly replicable, access and winning are the only edges that are hard to copy.

- Several FoFs are already moving in this direction. The conversations in this essay make that clear. But there’s no obvious leader yet. No name that’s synonymous with platform-level LP support the way a16z is synonymous with platform-level VC support. That position is still open.

- Taking it requires conviction, time, and resources. But AI is compressing the cost of building LP infrastructure in ways that weren’t true 3 years ago. And the allocators who figure out their specific edge will have a durable advantage that compounds across vintages.

- The metrics will eventually tell the story. Fundraising velocity, fund size vs. target, inbound ratios, LP base quality at Fund II – these numbers will accumulate over time and either validate the model or not. The FoFs building this data now will be the ones with the strongest argument when the question gets asked at scale.

I’m curious what you think. Who’s building this? And who do you think will be the first platform-based fund of funds that emerging managers talk about the way founders talk about the best VCs?

Subscribe to Signature Block

The data revolution in venture capital

Investors, data scientists, and tool builders leading the data-driven future of venture capital.